The main driver of cryptocurrency sentiment and price trends this week was not something endogenous to the crypto asset market, but rather a sharp geopolitical “black swan” event that shook both traditional markets and cryptocurrencies.

President Trump’s January 18 announcement that he would impose 10% tariffs on major European allies conditional on the US’ acquisition of Greenland triggered a violent risk-aversion event across all speculative categories. Bitcoin, which had been consolidating around the psychological $96,000 handle, experienced a “liquidity flush” and liquidated nearly $900 million in leveraged longs as the market pivoted to traditional safe-haven assets. However, the subsequent successful IPO of BitGo on the New York Stock Exchange suggests that, although short-term price movements remain sensitive to macro shocks, the structural institutionalization of the asset class is reaching a terminal velocity that is difficult to reverse.

Important points

Geopolitical Sensitivity: BTC’s temporary decoupling from “digital gold” status during the tariff announcement highlights BTC’s current role as a high-beta liquidity proxy rather than a pure geopolitical hedge. Gold’s jump to $4,800 highlights the ‘preference for physical’ amidst NATO-centric instability.

Infrastructure Legitimacy: BitGo IPO (ticker: BTGO) is priced above its implied valuation of $2.08 billion and marks the end of “cryptocurrency discounts” for regulated service providers. The support from Goldman Sachs and Citi is the seal of approval needed for the next wave of capital.

Regulatory standstill: Delays in the CLARITY Act in the Senate Banking Committee are a tactical setback for first-quarter optimism. The shift toward housing affordability suggests that the “crypto summer” that brings legislative certainty may be delayed into late spring.

Macro and market structure

liquidity system

We are currently navigating a complex volatility situation. Although global M2 money supply growth has stabilized at approximately +1.0% on a three-month rolling basis, the “cost of carry” for institutional investors remains elevated. The Fed’s current stance, complicated by the criminal investigation into Chairman Powell, has introduced a political risk premium to Treasury yields. We view the current environment as a “tug of liquidity”. Expansionary fiscal policy is combating risk-off sentiment caused by the escalation of the trade war.

Asset performance this week

( crypto-widget Coin=”bitcoin” link=”https://99bitcoins.com/goto/bestwallet” text=”Buy with Best Wallet” ), ( crypto-widget Coin=”ethereum” link=”https://99bitcoins.com/goto/bestwallet” text=”Buy with Best Wallet” ), Amid market uncertainty, most altcoins have been outflows this week. Bitcoin was down 5.23% from its price, Ethereum was slightly worse at -12.22%, and the crypto market cap was down just under 7%.

January 18 January 22 Bitcoin rate of change

$93,635

$88,737

-5.23

Ethereum

$3,347

$2,938

-12.22

Total market capitalization

$3,360,736,914,106

$3,130,345,656,216

-6.86

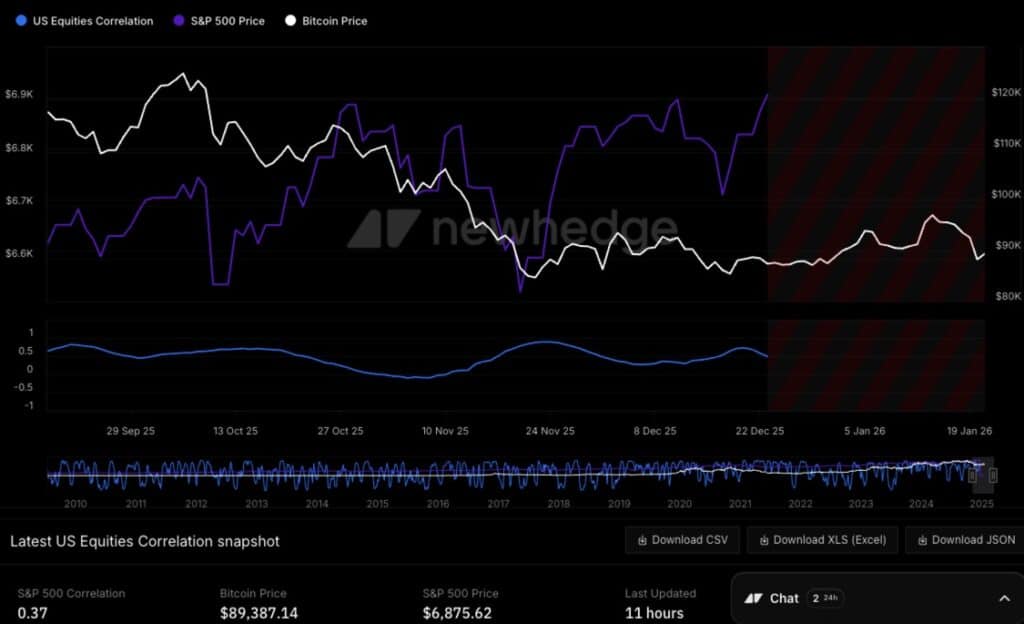

Observing correlations

The 30-day correlation between Bitcoin and the S&P 500 soared to 0.37 due to the simultaneous decline in “risk-on” assets following the tariff news. Conversely, the correlation with gold reversed this week to -0.15. This is because the yellow metal absorbed the safe-haven flows that Bitcoin failed to capture during the first two-hour plunge to $3,600.

Technical: Majors

Bitcoin: ETF cost-based test

The $91,000-$92,000 zone is more than just a technical level. This represents the estimated total cost basis for the 2025 Institutional Investor Cohort (the “ETF Class”). While the spot price declined to $91,900, we observed aggressive “tough buying” by authorized participants, but this was not enough to prevent further breaches below the $90,000 level. Basis trading remains profitable, but a contraction in the price of Kimchi Premium in South Korea amid a government investigation into the missing bitcoins signals a cooling of retail enthusiasm in the Asia-Pacific region.

Bitcoin could break below the weak trend line and fall to the next major support level at 84,000.

Ethereum: L2 value acquisition dilemma

Ethereum continues to face a fundamental identity crisis regarding value generation. Although network activity is at an all-time high, L2 Value Capture remains an issue for mainnet stakeholders. Approximately 88% of this week’s trading revenue was held by Arbitrum, Base, and Starknet, pushing Ethereum mainnet fees to a 12-month low. ETH will likely continue to underperform BTC on a risk-adjusted basis until the “burn rate” from the L1 blob is adjusted by EIP-7762 (expected in late 2026).

Sector in focus: AI and the agent economy

We are closely monitoring the influx of agents (capital controlled by autonomous AI agents). This week, we tracked over $140 million in on-chain volume generated by “heuristic arbitrageurs,” AI entities that operate without human intervention on the Solana and Base networks.

DePIN matures: Distributed computing-focused projects (Akash, Render, etc.) saw a 12% increase in usage this week as centralized GPU providers faced potential fee-related supply chain disruptions.

“River” bet: Justin Sun’s $8 million injection into River DeFi project is a play on “chain abstraction.” By integrating sTRX yield with stablecoin infrastructure, Sun seeks to capture liquidity for “unbanked” AI agents who require a fast, low-cost payment layer.

All of this has led to growing bullish sentiment around the crossroads of AI and the crypto economy and the possibility of a long game, but it’s worth warning that if this AI hype is anything like the dot-com boom, more than 90% of early projects will fail and eventually come to nothing.

My take: It’s too early to pick a long-term winner for DePIN AI, but it certainly has the potential for an interesting trade in the short term.

On-chain intelligence

Stablecoin speed: The speed of USDT on the TRON network increased by 18% this week. Elliptic’s report on Iran’s $500 million USDT acquisition suggests that stablecoins are increasingly being used for “sanctions-neutral trade.” While this creates regulatory headwinds, it also demonstrates the ‘asymmetric utility’ of this asset class.

Currency Flows: We noted the significant outflow of BTC from centralized exchanges to cold storage during the $91,900 plunge, suggesting that the “smart money” views Greenland’s decline as a volatility event rather than a reversal of a structural trend. We analyzed this behavior as a “flight to safety” amidst increasing geopolitical turmoil, and Bitcoin holders rushed to pull their coins from exchanges, but as soon as President Trump ruled out the use of force and eased EU tariffs, Bitcoin flows into exchanges increased.

The return to exchanges likely signals investors’ expectations that Bitcoin will return to around $97,000, where significant selling pressure is expected.

Regulation and policy oversight

Delay in the “clarity law” is the headline here. The Senate’s shift in focus to housing affordability suggests that the “Trump pump” on crypto legislation is cooling. AI, tariffs, geopolitical turmoil, and the Trump administration’s focus on affordability for Americans are shifting some of the attention away from the crypto bill. However, despite the Clarity Act’s delay, we do not expect a return to the “Gensler-era” attacks on cryptocurrencies, as Mr. Atkins sits at the top of the SEC and has already shown himself to be a cryptocurrency forward, although it is unclear how the jurisdictional relationship will play out between the SEC and the CFTC until the Clarity Act is introduced.

Meanwhile, the GENIUS Act remains the only solid guardrail for stablecoin issuers, which explains why BitGo’s IPO was greeted with such enthusiasm. They are one of the few companies with the necessary “compliance moat” to weather the current impasse.

Upcoming upcoming events

CME altcoin launch (February 9th)

The addition of Cardano (ADA), Chainlink (LINK), and Stellar (XLM) to the CME derivatives suite on February 9th is the next big structural tailwind. We expect “frontline” liquidity to shift to LINK, especially given its role as the leading oracle for the RWA (Real World Assets) sector. It would not be surprising to see that this is a “selling news” event, with price increases occurring in the days leading up to the event, followed by weak selling.

Disclaimer: This report is for informational purposes only and does not constitute financial, investment, or legal advice. Digital assets are subject to extreme volatility and risk of total loss. Please consult a qualified professional before making any investment decisions.

The post Weekly Crypto Market Update from January 18th to 22nd appeared first on 99Bitcoins.