Disclosure: The opinions expressed in this article are solely those of the author and do not reflect the views of crypto.news editorial team.

In a previous discussion about the tokenization of real estate, we highlighted how this innovative concept has struggled to gain traction, despite initial enthusiasm regarding its possibilities. The reality is that tokenization will remain a niche practice unless there is a solid economic foundation driving it. Unfortunately, widespread acceptance has not yet been achieved due to the lack of a compelling economic case.

I have been a proponent for years advocating for blockchain-based real estate registries featuring title tokens that authentically represent property rights, rather than merely serving as securities or investment notes. Although governments have been hesitant to adopt this concept, I have continued to delve into how tokenization can realistically benefit the real estate sector.

I recently encountered a groundbreaking idea that combines tokenization with decentralized finance (DeFi), leading to what I have termed IVVIA. The name is inspired by the Latin phrase “IV via,” meaning “fourth way,” and it proposes an exciting new method for obtaining real estate.

Introducing IVVIA: The Fourth Method

We are familiar with the conventional methods to purchase real estate: paying cash, securing a mortgage, or leasing. Each of these options has its drawbacks. For many, cash purchases are impractical, mortgage agreements entail long-term obligations and hefty fees, and leasing offers no pathway to ownership or return on investment. So, what if there was an alternative combining the advantages of ownership and investment with the flexibility of tokenization?

IVVIA’s concept is straightforward. A real estate buyer, referred to as an “ivviator,” can gradually purchase a home by acquiring tokens that symbolize ownership of a property. This resembles a mortgage in that the buyer makes monthly payments, but is less restrictive than a traditional bank loan. Instead, ivviators collaborate with real estate investors known as “ivviatees,” who possess the tokens. Over time, ivviators can buy these tokens at prevailing market prices, akin to repaying a mortgage, but with greater adaptability and reduced costs.

In contrast to a mortgage, where individuals are bound to a lengthy financial contract, IVVIA offers the opportunity to acquire tokens at one’s own pace. For instance, if an ivviator needs to relocate, they can sell their accumulated tokens at current market value and move on. For investors, this structure provides liquidity, as they can sell their tokens to ivviators or on the open market whenever they choose.

This entire process operates through smart contracts that streamline various daily transactions, from token purchases to monthly rental fees. The appeal of this model hinges on its flexibility and transparency, all facilitated by blockchain technology.

IVVIA Economics: Real-World Applications

To evaluate the practicality of this idea, I analyzed two decades of historical data from the Australian Bureau of Statistics, looking at factors such as property values, mortgage rates, rental costs, and bank interest rates. I modeled potential outcomes for both conventional mortgages and the IVVIA framework, and the findings were enlightening.

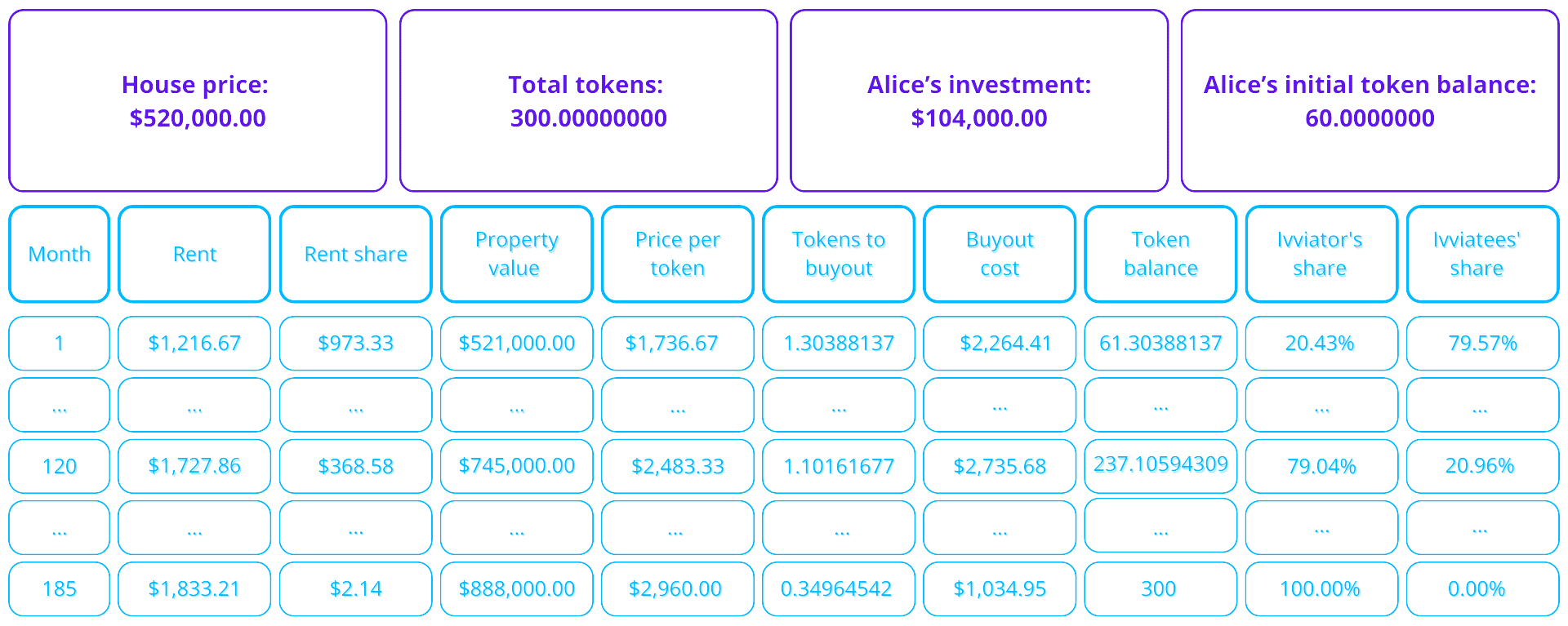

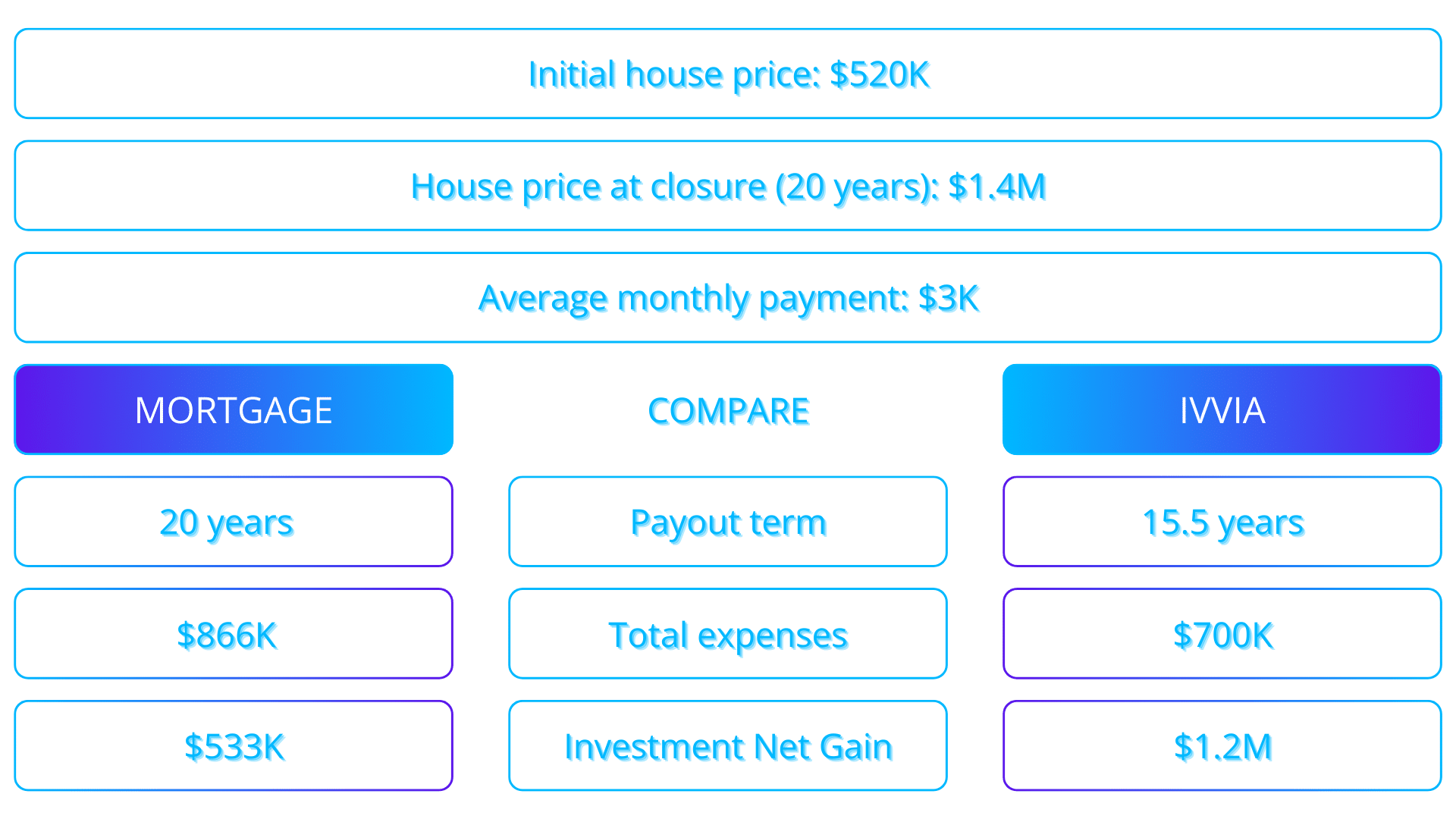

Consider Alice, who bought a two-bedroom house in Auburn, a suburb of Sydney, in 2004 for $520,000. She made a down payment of $104,000 (20%) and secured a 20-year mortgage with an average interest rate of 6.44%. Thus, her monthly payments amounted to $3,175. By 2024, she would have spent a cumulative $866,000 in total expenses—including both loan interest and the property’s value. If Alice sold the property then, she would have a net gain of $533,000 after deducting her total costs from the selling price of $1.4 million.

Now, let’s compare this process using the IVVIA approach. Instead of taking out a mortgage, Alice collaborates with four investors: Bob, Chuck, Dave, and Eve, each contributing $104,000 (matching Alice’s down payment). They form a unit trust to purchase and tokenize the property, sharing the tokens equally.

In this arrangement, Alice continues to make monthly payments that align with her $3,175 mortgage repayment. However, instead of paying back a bank loan, she allocates these funds to renting from her co-investors and purchasing their tokens.

This is how it works: Initially, Alice pays rent to her investors based on their property ownership percentages. If she owns 20% of the tokens, she would contribute 80% of the rent to the other investors. Assuming the property commands a market rent of $1,216 per month, Alice’s rent portion would be $973 (80% of the total). The remainder, $2,202 of her monthly limit, is dedicated to acquiring tokens from her co-investors at the current market price of the property.

In the first month, Alice is able to buy 1.30 tokens at the current value of $521,000, raising her ownership to 20.44%. As she accumulates ownership over time, her rent payments decrease. Fast forward ten years, and she’s nearing 79% ownership of the property, with her monthly rent having reduced to only 21% of the market rate ($368 per month). At that time, with the house’s value increased to $745,000, Alice is purchasing about 1.1 tokens monthly.

In just over 15 years, Alice will own the property outright, having invested a total of $700,000 (including the initial down payment, rent, and token purchases), which translates to a remarkable savings of around $166,000 compared to a traditional mortgage.

Investors’ Perspective

From the investors’ viewpoint, their experience is similar to that of Alice with a mortgage. Through IVVIA, they benefit from both rental income and the price appreciation between the original token price and its eventual sale price, starting from the month following the home purchase. Basic calculations suggest that their $104,000 investment could yield total returns of approximately $44,000.

For fair comparisons with traditional mortgages, certain conditions need to be in place. While IVVIA allows investors to earn monthly cash flow, conventional home loans lock part of household income into monthly payments for 20 years, effectively restricting access to equity. Thus, if Bob, as one of the investors, saves his rental or token sale proceeds like a homeowner would with equity, by the end of 20 years, he could accrue around $1,200,000. That’s 140% more than Alice’s gain of $533,000 under a traditional mortgage scenario.

From Idealistic Theories to Tangible Solutions

While IVVIA presents a viable solution to the challenges of real estate tokenization, there are significant obstacles to consider. Long-term real estate investments can encounter legal hurdles, such as disputes, insolvencies, or even issues stemming from the death of an owner. Basic smart contracts may not adequately address these complexities.

As IVVIA develops, it will require a dedicated smart contract administrator to oversee operations, navigate legal intricacies, and ensure compliance with evolving regulations. Despite these challenges, the efficiencies brought about by automation and decentralization create a system that is significantly more effective than traditional real estate financing.

Though real estate tokenization isn’t a novel idea, IVVIA introduces a genuine economic solution. By merging the versatility of tokenization with the reliability of real estate, it addresses the barriers that have kept real estate tokenization from reaching the mainstream. This initiative transcends mere blockchain applications; it signifies a transformational shift in our understanding of property ownership and investment.

IVVIA effectively aligns the incentives of buyers and investors and provides a flexible pathway to homeownership, all while transforming real estate into a dynamic, tradable asset. Through the use of smart contracts, DeFi principles, and fractional ownership, IVVIA holds the potential to redefine the landscape of real estate. This fourth method may indeed pave the way for a new standard in property acquisition.