Reasons to trust

Strict editing policy focusing on accuracy, relevance and fairness

Created by industry experts and meticulously reviewed

The highest standard for reporting and publishing

Strict editing policy focusing on accuracy, relevance and fairness

Morbi Pretium leo et nisl aliquam Mollis. Quisque Arcu Lorem, Ultricies Quis Pellentesque Nec, ullamcorper eu odio.

Español.

Bitcoin surged by more than 8% on Wednesday, reaching a high of $83,588 after President Donald Trump announced a 90-day suspension on new mutual tariffs in more than 75 countries except China. Investors and market analysts view the move as a relief signal, reflecting the hope that at least temporarily, the rapid escalation of tariffs will waned. But President Trump simultaneously hiked China’s tariff rate to 125%, indicating that the trade battle between the two biggest economies in the world is far from a solution.

Trump’s decision to suspend most of his newly announced tariffs was linked to concerns over a disruptive change in the bond market. Yen Treasury bond yields, which surged to seven-week highs, remained up after a tariff suspension was announced. Despite the temporary relief of many countries, immediate tariff hikes in China highlight an ongoing stalemate and suggests sustained uncertainty in the global market. Some analysts believe the surge in risky assets, including Bitcoin, is driven in part by changing expectations regarding future negotiations.

Potential China is not the price of Bitcoin

In this background, founder, CEO, CIO, and SOLO Management GP of Crypto Fund’s asymmetric GP, Joe McCann, expressed his perspective on X, observing that the market is originally pricing for tariffs in China, the EU and worldwide, but now only in China.

Related readings

He showed that the market will explode higher if a breakthrough emerges as the deal with Beijing remains priceless.” “The market was priced so that China, the EU and everyone else had tariffs. Currently, the market is priced only in China. The market is not priced for Chinese trades,” McCann said.

He also noted that “explosions at the long edge are explosions of the risk parity pod,” referring to the rapid market movement in long term bonds. McCann sees the current environment as reminiscent of the market bottom during the community, with funds beginning to cover positions and short term periods. He highlights the possibility that if the yuan is strengthened against the dollar, it could mean that China is ready to negotiate, implying that fairness and crypto markets could be too low in trade.

“Today, only long funds are grossed again, shorts are covered. Trump is willing to signal China’s biggest pain and negotiate. The market can only have a higher price. If Yuan gathers against tonight’s dollar, it’s likely a sign that China wants to negotiate.

“I haven’t left the forest yet.”

Jeff Park, head of Alpha Strategies at Bitiwise, warns that the environment remains vulnerable, weakening the original dynamics at X, noting that 10-year yields above 4%, and ongoing credit concerns at spreads above 400 basis points persist in potential reverse motion. According to him, “(This would be) an unpopular opinion (…) we are still out of the woods (…) the net outcome is still negative for risky assets, especially if the Federal Reserve does not cut interest rates as previously expected.”

Related readings

He cited this lack of financial support as a factor that amplifies volatility. “I’m actually more concerned about how little liquidity in the market is to experience this casino swing, if any,” he writes via X.

X user Adam Yoder agrees, “The bonds are still up today and money has risen.” “This is actually a scary move,” Park suggested, expressing confusion over what the White House hopes to achieve with a partial pause that leaves China alone to take the brunt of the brunt.

Meanwhile, in a quick turnaround in the previous call, Goldman Sachs retracted its recently announced recession baseline after a 90-day suspension was confirmed. The revised outlook issued by Jan Hatzius argues that while gross duties (both existing 10% and the expected sector-specific 25%) are still in place, the market is sparing immediate global escalation.

Goldman returns to his previous non-reducing baseline forecast of 0.5% Q4/Q4 GDP growth in 2025, a 45% chance of a recession, and three consecutive 25 basepoint “insurance” reductions in June, July and September. “We continue to look forward to additional sector-specific tariffs,” according to the statement, and an overall rate was expected to approach the 15% point increase that Goldman had initially anticipated.

I’m looking at today’s CPI release

In particular, today, the US Consumer Price Index (CPI) data for March 2025 is scheduled to be released by the US Bureau of Labor Statistics (BLS) at 8:30 ET.

The February 2025 CPI showed an increase in the previous year (Yoy) year-on-year (unseasonally adjusted) year-on-year, with a 0.2% increase in the month (moms) over the course of the year. Core CPI, excluding food and energy, increased by 3.1% year-on-year. This shows slight cooling from the 3.0% year-over-year heading rate in January, suggesting a gradual developmental trend.

Expectations for CPI in March would potentially fall to around 2.5%, with some analysts suggesting that if trends in housing costs, rent and energy prices continue to ease, they could fall below 2.6%. Core CPI is expected to hover around and around 3.0% to 3.1%, reflecting sustained pressure from service and shelter costs.

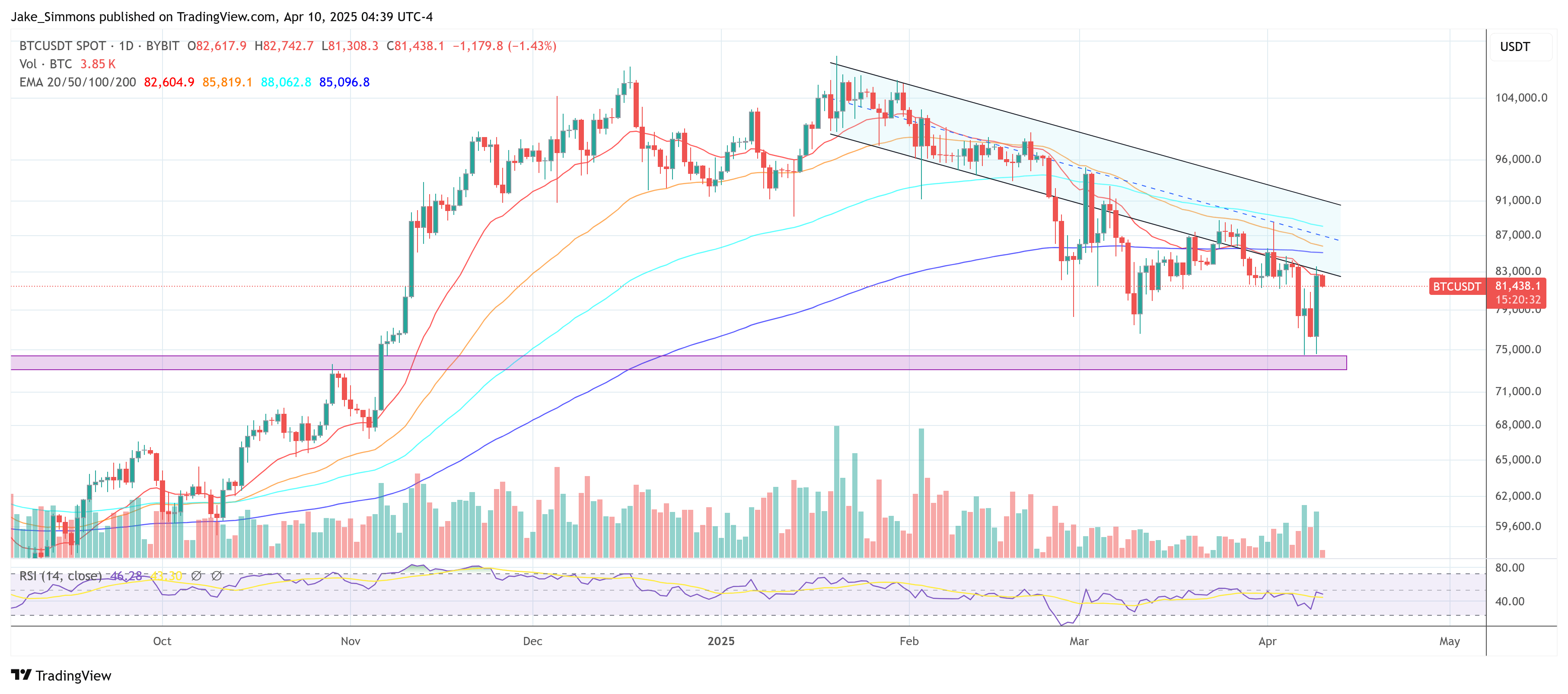

At the time of pressing, BTC traded for $81,438.

Featured images created with dall.e, charts on tradingview.com